How To Calculate Cap Rate: Calculator, Formula, & FAQs

Feb 19, 2025

The capitalization rate helps determine whether or not a deal’s rate of return and potential profitability is worth the initial investment; it is quite literally a calculation that attempts to tell investors if they should invest in a particular opportunity.

Trust us--there are plenty of options property investors will want to analyze with an easy-to-use cap rate calculator.

That said, nobody will teach you how to calculate the cap rate for real estate if you don’t ask; you need to be proactive and translate the information you come up with into actionable steps.

Instead of relying on others, we’ve developed a free cap rate calculator for our readers to use!

Along with our calculator, this guide will tell you everything you need to know about cap rates, including:

- Use Our Free Cap Rate Calculator

- What Is Cap Rate?

- How Does A Cap Rate Calculator Work?

- The Role Of Cap Rate In Investment Properties

- What Is The Cap Rate Formula?

- How To Calculate The Cap Rate

- Cap Rate Formula Examples

- Impact of Net Income on Property Value

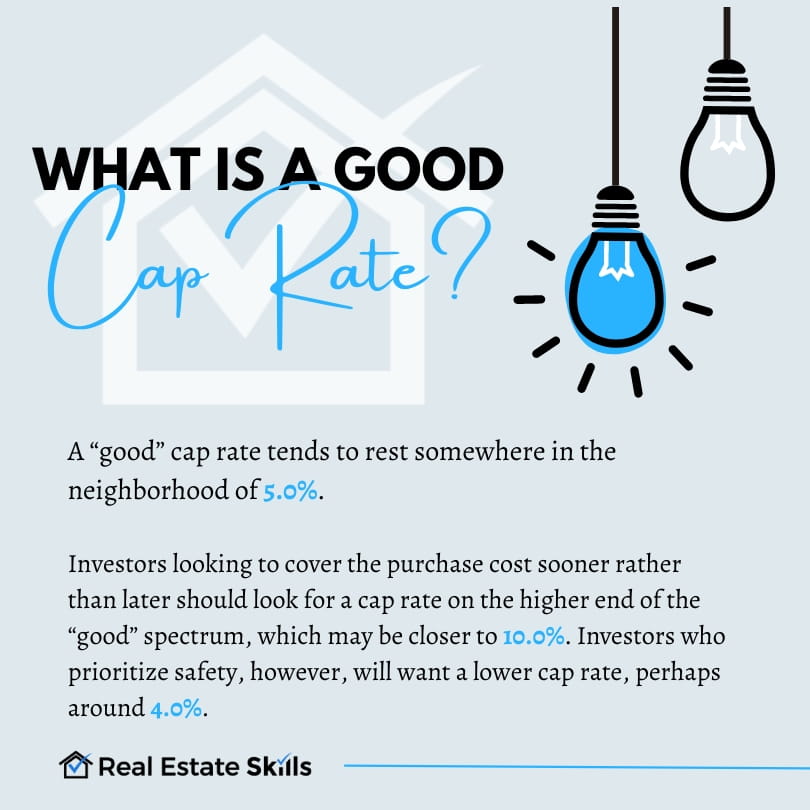

- What Is A Good Cap Rate?

- Limitations Of Capitalization Rate

- Capitalization Rate: Frequently Asked Questions

- Final Thoughts On Cap Rate Calculators

Ready to Take the Next Step in Real Estate Investing? Join our FREE live webinar and discover the proven strategies to build lasting wealth through real estate.

Whether you're just getting started or ready to scale, we'll show you how to take action today. Don't miss this opportunity to learn the insider tips and tools that have helped thousands of investors succeed! Seats are limited—Reserve Your Spot Now!

Cap Rate Calculator

Quickly & Easily Analyze Your Investment Properties

This cap rate calculator provides a quick estimate of a property's capitalization rate, but accuracy depends entirely on the numbers you input. Be sure to use precise figures for net operating income (NOI) and property value to get the most reliable results. While this tool gives you a strong starting point for evaluating rental property investments, it’s essential to conduct thorough due diligence. Investors who input accurate data will gain a clearer understanding of their property's potential return. Use this cap rate calculator as a guide, but always verify your numbers before making investment decisions.

What Is Cap Rate?

The capitalization rate, or cap rate, is an invaluable metric that can help quantify the expected rate of return on commercial investment properties (not unlike apartment buildings). As a result, the real estate investing community has come to rely on cap rates to analyze deals and compare potential returns before following through with a purchase.

On the surface, cap rate is one of the best ways for real estate investors to determine whether or not a deal is worth pursuing. A properly calculated cap rate can estimate a property’s rate of return.

However, a cap rate should only complement a comprehensive and detailed analysis of the subject property; it’s not designed to stand alone.

If for nothing else, the cap rate is an approximation, not a definitive value. Nevertheless, despite their inherent inefficiencies, cap rates are an invaluable tool for an experienced investor.

How Does A Cap Rate Calculator Work?

A cap rate calculator is used to measure a subject property's expected rate of return.

As its name suggests, a cap rate calculator will help turn relative variables into quantifiable values expressed as a percentage. The percentage resulting from the calculation will give investors an estimated return on investment (ROI).

Try out our free cap rate calculator above to get a close estimation of your ROI.

Why Use A Cap Rate Calculator?

Using a cap rate calculator takes the guesswork out of analyzing rental properties. By inputting net operating income (NOI) and the current market value, investors can determine whether a property aligns with their investment goals. However, accuracy is crucial—the results are only as good as the numbers entered.

While a cap rate calculator offers a solid estimation, investors should also consider additional factors such as market conditions, property appreciation, and financing costs before making decisions.

Try out our free cap rate calculator above to get an accurate estimation of your return on investment (ROI) and make informed real estate investment choices!

Read Also: How To Calculate ROI On Rental Property

The Role Of Cap Rate In Investment Properties

Cap rate is more than just a number—it’s a fundamental metric that helps shape real estate investment strategies. Investors use capitalization rates to assess potential returns, compare properties, and determine whether a deal aligns with their financial goals.

A higher cap rate often signals a higher potential return, but it also tends to come with greater risk—such as properties in less stable markets or those requiring significant repairs. On the other hand, a lower cap rate typically indicates a safer investment with more predictable cash flow but lower overall returns.

By using our cap rate calculator, real estate investors can analyze different properties, balance risk and reward, and make more informed investment decisions. Whether you're looking for high-yield rental properties or long-term appreciation, understanding your cap rate helps you tailor your strategy to match your risk tolerance and return expectations. Try our free cap rate calculator above to evaluate your next investment!

What Are Capitalization Rates Used For?

Cap rates are most commonly used for estimating the returns on investment properties. Upon a closer look, however, the metric is more versatile than most people give it credit for. In addition to estimating returns, cap rates may be used in the following ways:

- Reverse Engineer Valuations: Investors may calculate the cap rate if they have the NOI and the value of the property. However, what if the market value isn’t available? If investors can access the cap rate and the NOI, they can estimate a property’s valuation with a similar calculation (NOI/cap rate = property value estimate).

- Compare Similar Properties: If investors are torn between similar investments, the cap rate can help determine which of the real estate comps to choose. Pitting two properties’ cap rates against each other will reveal which investment will likely produce more returns relative to its purchase price.

- Assess Risk: Calculating cap rate metrics can give investors a better idea of the risk associated with the property. All else being equal, a property that returns less capital relative to its purchase price is riskier than a property that returns more. Therefore, comparing the cap rates of two similar subject properties can tell investors which represents the more significant risk.

- Loan Approvals: If lenders know the subject property being purchased is for investment purposes, they may use the cap rate to evaluate a borrower’s risk profile. Anything a lender can use to assess the risk of a loan will ultimately change the underwriting, which can impact the terms of the impending loan.

Read Also: The Ultimate Guide To Real Estate Investment Calculators (And How To Use Them Like a Pro)

What Is The Cap Rate Formula?

Alex Martinez, the founder of Real Estate Skills, is known for his strong, practical expertise in real estate, starting from a beginner with no family connections in the industry to completing over 50 real estate deals, including wholesale and flips, within his first year.

He has dedicated his career to providing cutting-edge education and resources for real estate professionals. He emphasizes the importance of self-taught knowledge through mentors, books, and hands-on experience.

His journey from earning a modest income to becoming a successful real estate entrepreneur and educator showcases his expertise and dedication to the field.

Ryan Zomorodi, co-founder and COO of Real Estate Skills, leverages his experience from a diverse background in real estate investment, construction management, and entrepreneurship to provide comprehensive education in the real estate sector.

His expertise is rooted in hands-on experience, extensive industry knowledge, and a commitment to empowering others through education.

Ryan's journey reflects a blend of practical experience and entrepreneurial success, contributing to his role in developing a platform that educates and supports aspiring real estate professionals.

Read Ryan's Full Bio >>

How To Create Wealth Through Real Estate Investing

Consistently Close Deals WITHOUT Any Experience, WITHOUT Using Your Own Money, & WITHOUT Working 40+ Hours/Week!

We recommend Colibri Real Estate School for getting licensed. Click the button below to get started!